All Categories

Featured

Table of Contents

As a leading company of annuities, the condition quo isn't a condition we ever before desire. We'll constantly be in search of much better. If you are a non-spousal recipient, you have the choice to put the money you inherited right into an acquired annuity from MassMutual Ascend! Inherited annuities may provide a method for you to spread out your tax obligation obligation, while permitting your inheritance to continue growing.

Your decision might have tax obligation or various other effects that you may not have actually taken into consideration. To aid prevent surprises, we suggest talking with a tax obligation advisor or a financial professional prior to you choose.

How does Annuity Interest Rates inheritance affect taxes

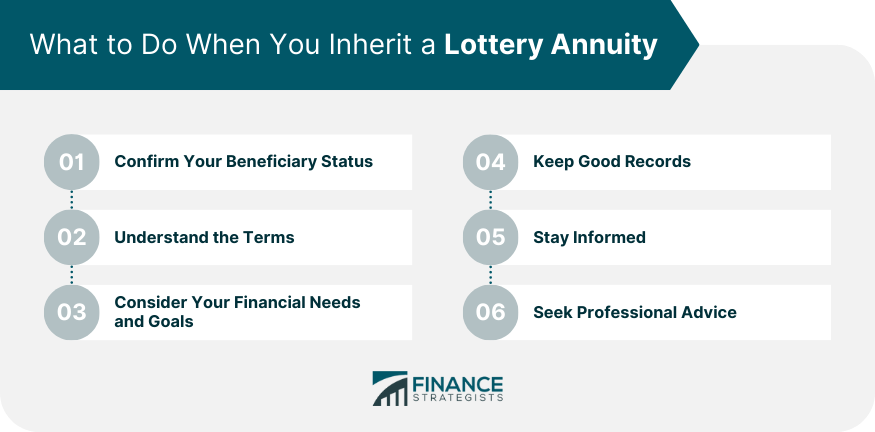

Annuities don't constantly follow the same rules as various other properties. Lots of people turn to annuities to take benefit of their tax obligation advantages, as well as their one-of-a-kind capability to assist hedge against the economic risk of outliving your cash. When an annuity proprietor passes away without ever having annuitized his or her policy to pay routine income, the person called as recipient has some crucial decisions to make.

Allow's look much more very closely at how much you have to pay in taxes on an inherited annuity. For most kinds of residential or commercial property, earnings tax obligations on an inheritance are quite straightforward. The common instance involves assets that are eligible for what's called a boost in tax obligation basis to the date-of-death value of the acquired residential or commercial property, which efficiently erases any type of built-in resources gains tax obligation responsibility, and offers the successor a tidy slate against which to measure future revenues or losses.

Tax rules for inherited Variable Annuities

For annuities, the key to taxes is just how much the deceased individual paid to buy the annuity contract, and how much cash the departed person obtained from the annuity prior to death. IRS Magazine 575 claims that, as a whole, those acquiring annuities pay taxes similarly that the original annuity owner would.

In that situation, the taxes is much simpler. You'll pay tax obligation on every little thing over the cost that the original annuity proprietor paid. The quantity that stands for the original costs repayment is treated as tax basis, and as a result excluded from gross income. There is an unique exemption for those who are entitled to get surefire repayments under an annuity contract. Annuity payouts.

Above that amount, payments are taxed. This reverses the common rule, and can be a big advantage for those acquiring an annuity. Acquiring an annuity can be much more difficult than obtaining other residential or commercial property as a successor. By recognizing unique regulations, though, you can choose the least-taxed options offered in taking the cash that's been delegated you.

We 'd like to hear your inquiries, ideas, and viewpoints on the Knowledge Center in general or this page in particular. Your input will help us help the world spend, better! Email us at. Thanks-- and Deceive on!.

Are Tax-deferred Annuities death benefits taxable

When an annuity proprietor passes away, the remaining annuity value is paid out to people who have been called as recipients.

Nonetheless, if you have a non-qualified annuity, you won't pay revenue tax obligations on the contributions section of the circulations given that they have actually currently been strained; you will only pay income taxes on the profits part of the distribution. An annuity survivor benefit is a type of repayment made to a person identified as a recipient in an annuity contract, usually paid after the annuitant passes away.

The beneficiary can be a kid, partner, moms and dad, and so on. The quantity of death benefit payable to a beneficiary may be the amount of the annuity or the quantity left in the annuity at the time of the annuity owner's death. If the annuitant had actually started receiving annuity repayments, these payments and any type of appropriate costs are subtracted from the fatality proceeds.

In this situation, the annuity would offer an ensured fatality advantage to the beneficiary, no matter the staying annuity equilibrium. Annuity death advantages undergo earnings tax obligations, but the tax obligations you pay depend on just how the annuity was fundedQualified and non-qualified annuities have various tax obligation ramifications. Certified annuities are moneyed with pre-tax money, and this implies the annuity owner has not paid taxes on the annuity contributions.

When the survivor benefit are paid out, the internal revenue service considers these benefits as earnings and will certainly be subject to common earnings tax obligations. Non-qualified annuities are funded with after-tax bucks, significances the payments have actually already been strained, and the cash won't be subject to revenue taxes when dispersed. Any type of profits on the annuity contributions expand tax-deferred, and you will certainly pay revenue taxes on the earnings part of the circulations.

Taxation of inherited Annuity Interest Rates

They can choose to annuitize the contract and receive routine settlements with time or for the remainder of their life or take a round figure repayment. Each payment option has different tax implications; a round figure repayment has the highest possible tax effects given that the settlement can press you to a higher income tax brace.

You can likewise make use of the 5-year guideline, which lets you spread the acquired annuity repayments over 5 years; you will pay taxes on the distributions you get each year. Beneficiaries inheriting an annuity have numerous choices to receive annuity repayments after the annuity proprietor's fatality. They consist of: The beneficiary can decide to receive the staying worth of the annuity agreement in a single lump amount repayment.

This choice utilizes the beneficiary's life expectancy to identify the size of the annuity payments. It offers annuity repayments that the recipient is qualified to according to their life span. This regulation needs recipients to secure annuity payments within five years. They can take multiple payments over the five-year period or as a single lump-sum repayment, as long as they take the complete withdrawal by the 5th anniversary of the annuity proprietor's fatality.

:max_bytes(150000):strip_icc()/grat.asp-final-687dbf83454840fd857a94e53eb6172c.png)

Here are things you can do: As an enduring spouse or a departed annuitant, you can take ownership of the annuity and continue taking pleasure in the tax-deferred condition of an inherited annuity. This enables you to avoid paying taxes if you keep the money in the annuity, and you will only owe income taxes if you receive annuity repayments.

Nevertheless, the 1035 exchange only uses when you exchange comparable annuities. You can exchange a qualified annuity for another certified annuity with far better attributes. You can not exchange a qualified annuity for a non-qualified annuity. Some annuity contracts provide special riders with an boosted survivor benefit. This benefit is a bonus that will be paid to your recipients when they inherit the staying equilibrium in your annuity.

{kind=link}

Table of Contents

Latest Posts

Exploring the Basics of Retirement Options Everything You Need to Know About Immediate Fixed Annuity Vs Variable Annuity What Is the Best Retirement Option? Benefits of Choosing the Right Financial Pl

Exploring Variable Annuities Vs Fixed Annuities A Closer Look at Fixed Indexed Annuity Vs Market-variable Annuity Breaking Down the Basics of Fixed Annuity Vs Variable Annuity Advantages and Disadvant

Exploring Fixed Annuity Or Variable Annuity Everything You Need to Know About Financial Strategies Breaking Down the Basics of Indexed Annuity Vs Fixed Annuity Pros and Cons of Variable Annuities Vs F

More

Latest Posts